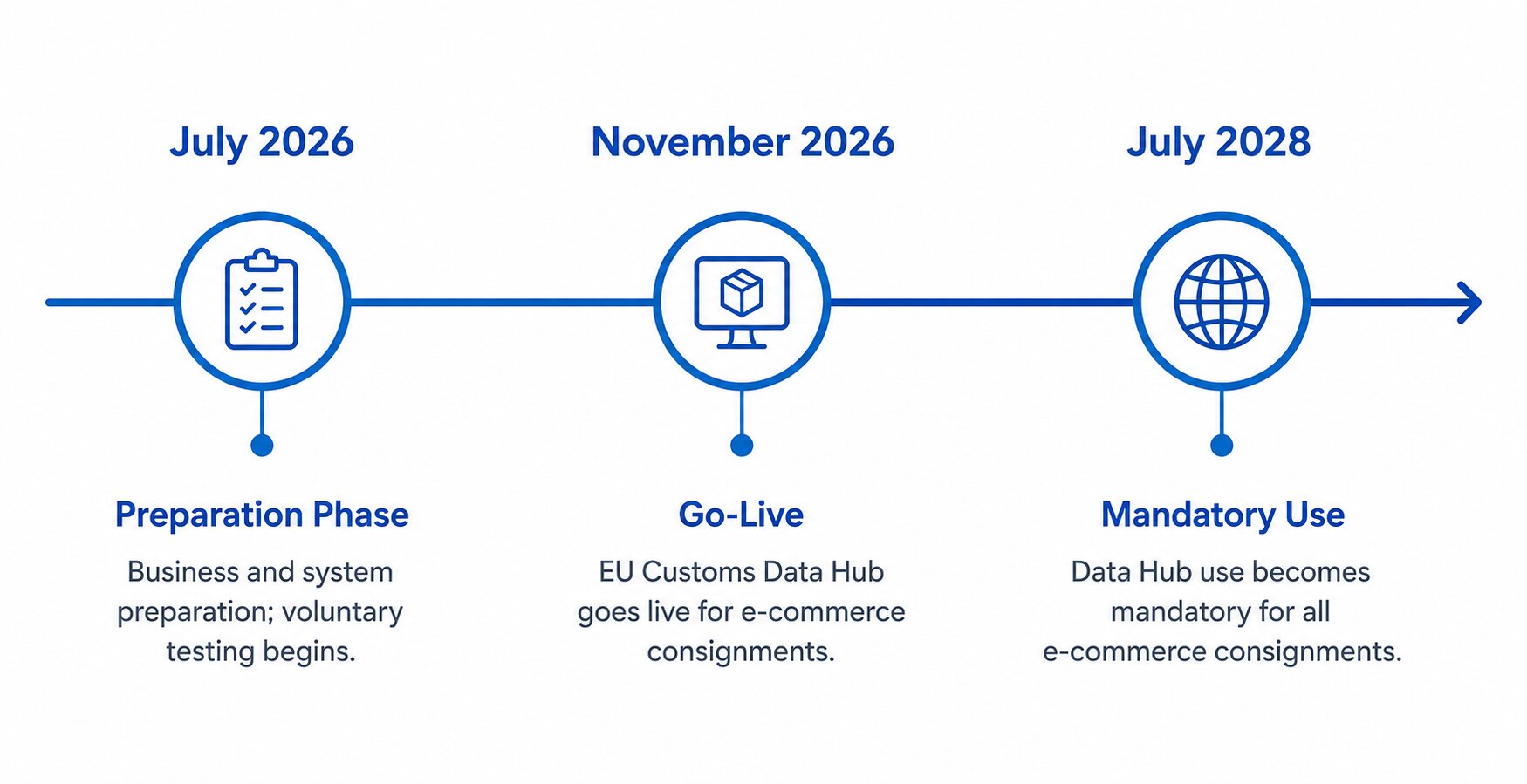

From 1 November 2026, EU Product Identifier (PID) requirements make a set of item-level codes mandatory on customs declarations for low-value B2C imports. Any consignment worth €150 or less, sold to a private buyer as a distance sale of imported goods, must now carry a Product Identifier for each item on the declaration (EU Taxation & Customs Union). The rule has been live on a voluntary basis since 1 July 2026, so the November date is when “optional” becomes “or your parcel waits at the border.” Up to three identifiers are involved: a merchant code, a manufacturer code, and, where the product has one, a standardised barcode number. Business-to-business shipments to VAT-registered recipients sit outside the requirement entirely. This guide explains what the three PIDs are, which shipments are actually caught, and what an importer or seller has to do before the deadline.

Key takeaways

- PIDs are a data requirement, not a charge. From 1 November 2026 they must appear at line-item level on customs declarations for B2C distance sales into the EU27 (European Commission). No PID, no clean clearance.

- Three identifiers, two of them mandatory. You supply a Merchant PID and a Non-Standardised Manufacturer PID; the Standardised PID (a GTIN/EAN/UPC barcode) is added where it exists (KPMG).

- B2B is exempt. Low-value imports to VAT-registered business recipients do not need PIDs. The requirement targets distance sales to consumers (FedEx).

- This is one piece of the €150 reform. PIDs ride the same overhaul that scrapped the €150 duty exemption and added a €3 flat duty on 1 July 2026 (Avalara). The duty and the identifiers are separate tracks.

Scope and audience: this explains the EU’s new Product Identifier rules for SME importers, non-EU sellers shipping to EU consumers, and the mixed B2B/B2C businesses in between. It covers what the three PIDs are, who must file them from 1 November 2026, and how to prepare. It is general guidance for freight and import planning, not tax or legal advice, and it does not cover the separate US de minimis change except as context.

On this page

- The short answer

- What a Product Identifier actually is

- Who this hits, and who it doesn’t

- Where PIDs fit in the 2026 reform

- What happens if the data is missing or wrong

- How to get PID-ready before 1 November

- Worked example: a €140 parcel

- FAQ

The short answer

A Product Identifier is a code that pins each item on a customs declaration to a specific product, and from 1 November 2026 the EU requires one for every line in a low-value B2C import. Before this reform, a sub-€150 parcel could clear on a loose goods description such as “cotton t-shirt” or “phone case,” and nothing tied that description back to a real catalogue entry. Customs could see the words but not the product. The PID closes that gap by carrying the seller’s own code and the manufacturer’s code straight onto the declaration, so the authority can match what was ordered, what was declared, and what is in the box.

The requirement has been optional since 1 July 2026 to let sellers and carriers test their data pipes (EU Taxation & Customs Union). That grace period ends on 1 November. After it, a declaration filed without the mandatory identifiers is incomplete, and an incomplete declaration is one a customs system can reject or hold.

What a Product Identifier actually is

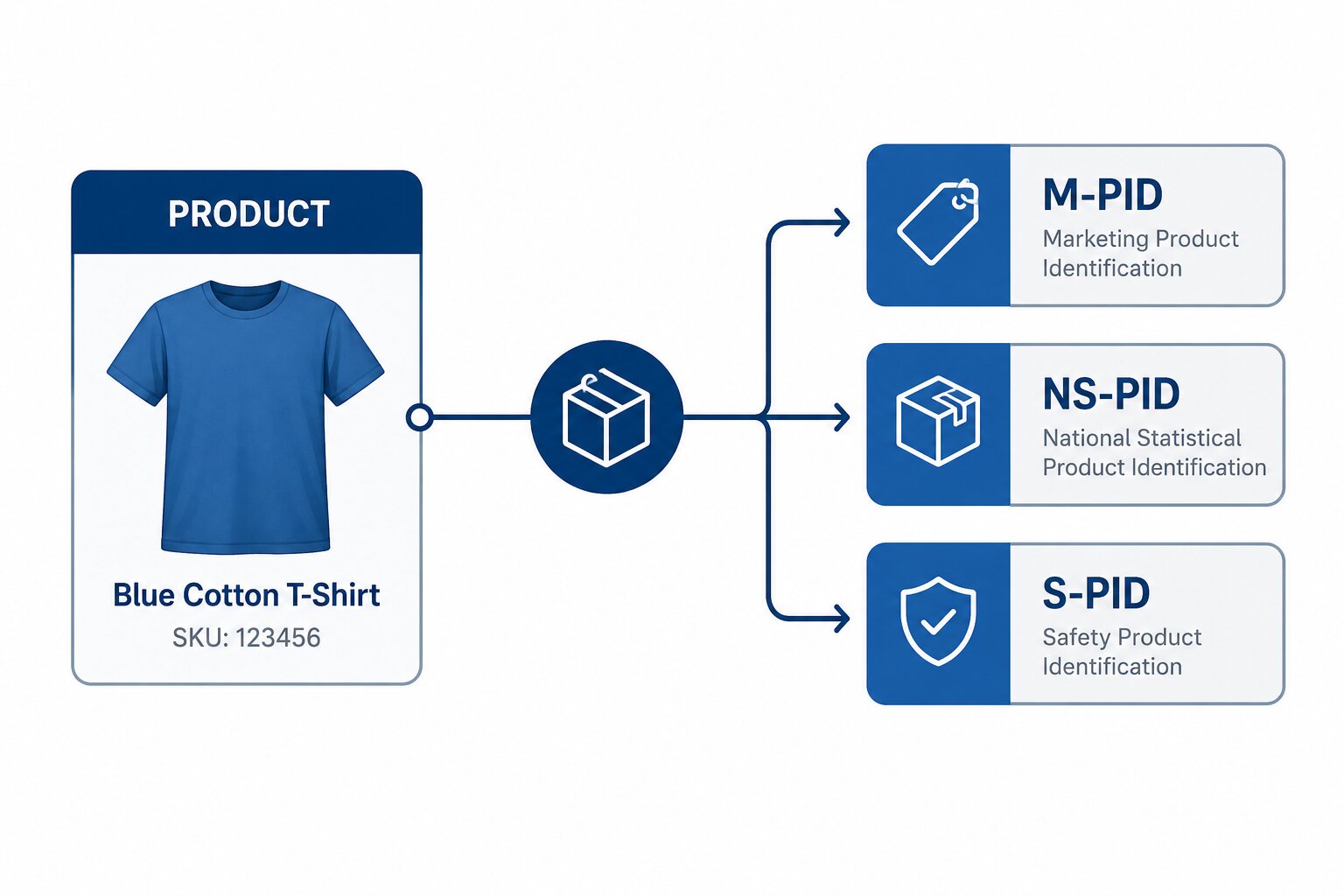

Three codes sit under the PID umbrella, and they answer three different questions: what does the seller call this item, what does the maker call it, and does it carry an industry barcode? Two are mandatory to file, the third is included when the product has one.

| Identifier | Short name | What it is | Example | Status from 1 Nov 2026 |

|---|---|---|---|---|

| Merchant Product Identifier | M-PID | The seller’s own internal code for the item | SKU TS-BLK-M, item code, product number | Mandatory |

| Non-Standardised Manufacturer PID | NS-PID | The manufacturer’s or supplier’s unique code for that product | Supplier article no. AC-4471 | Mandatory where it exists |

| Standardised Manufacturer PID | S-PID | A global-standard code carried on a barcode | GTIN, EAN, UPC, ISBN | Report where available |

The M-PID is the one nobody can dodge: it is simply your SKU, the code already sitting in your order system. The NS-PID is the supplier’s part number for the same item, the code on the purchase order or the factory’s spec sheet. The S-PID is the barcode number, the GTIN or EAN a scanner reads at a till; a mass-produced consumer product usually has one, while an unbranded, custom, or handmade item often does not (KPMG).

Where does a seller find these? The M-PID lives in your e-commerce backend. The NS-PID comes from your supplier’s catalogue or invoice. The S-PID is printed on the retail packaging, right under the barcode. The awkward truth for a lot of SME importers is that these three codes rarely sit in the same system today, which is exactly the readiness problem the rest of this guide deals with.

Who this hits, and who it doesn’t

The PID rule is narrower than the headlines suggest: it applies to B2C distance sales of imported goods in consignments valued at €150 or less. Put plainly, it targets the classic cross-border e-commerce parcel, where a private EU buyer orders from a non-EU shop and the goods ship in on a low-value declaration. That is the flow the reform was written for.

Two groups fall outside it. First, B2B imports to VAT-registered recipients are exempt from the PID requirement altogether (FedEx). If your customer is a registered business importing for its own use or resale, the identifiers are not required, and the shipment clears on the standard commercial track with percentage-based duty. Second, consignments above €150 already declare under full customs rules, so they were never the target of this low-value reform in the first place.

So which of our own clients does this actually touch? On the lanes we handle, a pure wholesale importer moving pallets to a VAT-registered EU company is unaffected. The businesses that need to act are the ones with a consumer-facing leg: an SME that sells to EU consumers through its own webshop or a marketplace, a dropshipper, or a brand that fulfils individual orders from a non-EU warehouse. If you run both B2B pallets and a B2C webstore, only the B2C line-items need PIDs, but “we do a bit of both” is precisely the profile that gets caught out, because the consumer parcels move on the same account as the wholesale freight. [case study placeholder: Sea Gate B2C-fulfilment client example]

Where PIDs fit in the 2026 reform

PIDs are the data half of a two-part change that began on 1 July 2026, and it helps to keep the two parts separate. On that date the EU removed the €150 customs-duty de minimis exemption and brought in a temporary €3 flat duty per item on low-value B2C consignments, a rate set to run until the EU Customs Data Hub goes live on 1 July 2028 (European Commission; Avalara). That was the money change: what a parcel now costs to import.

The PID requirement, four months later, is the identity change: how a parcel is described. One decides the charge, the other decides whether the declaration is complete enough to process. A seller can pay the €3 and still be stopped for a missing identifier, in the same way that prepaying VAT through IOSS never guaranteed a clean release either. If you are mapping the whole timeline, our guides on IOSS after de minimis and the EU Customs Data Hub coming in 2028 cover the duty and the 2028 endgame; this article is the piece in the middle.

Why bother with all this identity data? The Commission’s stated aim is a risk-based, data-driven border, one where customs can screen shipments against real product records instead of free-text descriptions, catch undervaluation and mislabelling, and eventually clear compliant goods faster (EU Taxation & Customs Union). PIDs are the raw material for that system.

What happens if the data is missing or wrong

A declaration without its mandatory identifiers is treated as incomplete, and incomplete declarations do not clear on time. In practice, the failure modes are mundane and expensive: a customs hold while the missing code is chased, a delivery delay measured in days, brokerage back-and-forth as the carrier requests the data, and, for the goods themselves, the risk of a penalty or a refused parcel that ships back at your cost (OpenGov Asia).

Inconsistent data is its own trap. If the M-PID on the declaration points to one product and the physical goods or the invoice say another, that mismatch is exactly what a risk-based system is built to flag. The identifiers have to be right, not just present. And because the codes now travel the full chain, from product master data to order system to shipping label to declaration to broker, an error introduced at any one step surfaces at the border rather than before.

There is also a carrier layer worth knowing. The requirement is landing unevenly across carriers: FedEx and UPS already ask for PIDs on EU B2C customs data, while some networks have been slower to enforce collection (metafour). Do not read a carrier’s silence as an exemption. The legal obligation attaches to the declaration from 1 November regardless of whether a given carrier has switched on the validation yet.

How to get PID-ready before 1 November

Getting ready is a data exercise, not a legal one. The work is making sure three codes exist for every product and reach the declaration cleanly. A practical sequence:

- Map your catalogue to the three fields. For each product you ship B2C into the EU, list its M-PID (your SKU), its NS-PID (the supplier’s article number), and its S-PID (the barcode/GTIN, if it has one). Spreadsheet first, system later.

- Fill the NS-PID gaps at source. The supplier code is the one most SMEs are missing. Ask suppliers for their part numbers now and store them against your SKUs. This is the single most common blocker.

- Decide what to do when there is no barcode. For unbranded, custom, or handmade items with no S-PID, that field stays empty; the M-PID and NS-PID still have to be there. Confirm your system leaves the S-PID blank rather than inserting a placeholder.

- Check the data actually flows to customs. Confirm the identifiers pass from your order platform to your carrier or broker and land on the declaration. Use the voluntary window before 1 November to send live shipments with PIDs and watch them clear.

- Confirm your carrier’s format. Ask each carrier how they want the fields populated in their shipping data, since FedEx, UPS, and others differ in where the codes go.

- Assign an owner. One person should own PID data quality. The codes touch product, warehouse, and shipping, so without a named owner the gaps reappear.

If you file through a forwarder rather than a courier portal, this is a conversation to have before the deadline, not on it. On the B2C lanes we handle we would rather map a client’s catalogue in October than clear a held parcel in November.

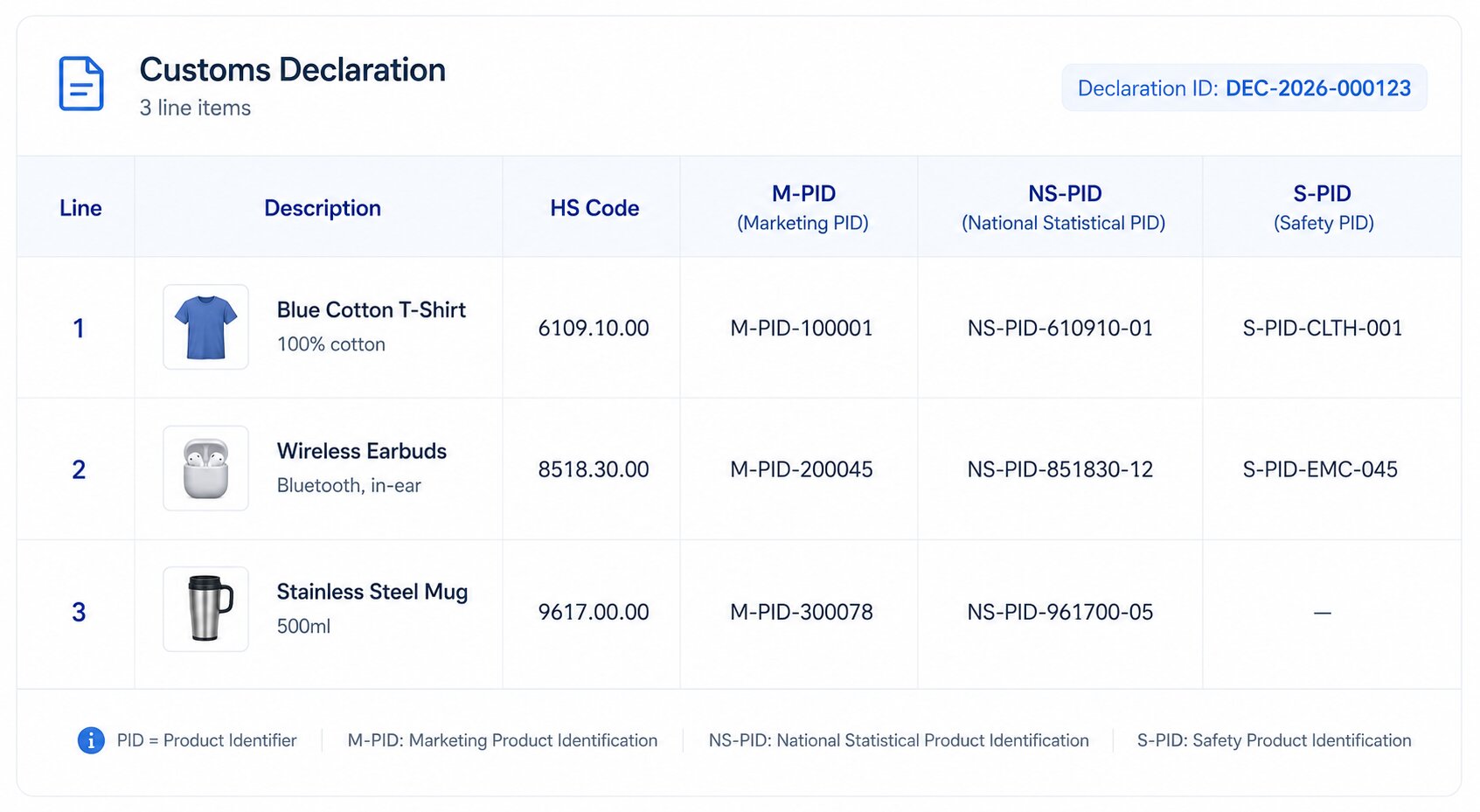

Worked example: a €140 parcel

Picture a €140 order shipped from a non-EU webshop to a consumer in Germany, three items in the box: a branded phone case, a plain cotton tote, and a supplier-made cable. Because it is a B2C distance sale at or under €150, every line needs a PID from 1 November 2026.

- Phone case: M-PID PC-IP15-BLU (your SKU), NS-PID AC-4471 (the maker’s code), S-PID 4012345678901 (its EAN barcode). All three present.

- Cotton tote: M-PID TOTE-NAT, NS-PID from the workshop’s article list; no retail barcode, so the S-PID stays blank. Two of three, which is compliant.

- Cable: M-PID CAB-USBC-1M, NS-PID from the supplier, S-PID 0885909950805 (its UPC). All three present.

The declaration lists three line items, each carrying at least its M-PID and NS-PID. Separately, the €3 flat duty applies to the consignment under the July reform, and that charge is paid regardless of the identifiers. Get the codes right and this parcel clears on the data; leave the cable’s supplier code blank and the whole shipment can sit while the carrier asks you for one number.

FAQ

What is a Product Identifier (PID) in EU customs?

It is an item-level code that links a line on a customs declaration to a specific product. From 1 November 2026 the EU requires PIDs on declarations for low-value B2C imports, so customs can match the declared goods to real product records rather than a free-text description.

When do EU PID requirements become mandatory?

Mandatory from 1 November 2026. They have been available voluntarily since 1 July 2026, a testing window meant to let sellers and carriers get their data pipelines working before enforcement begins.

What are the three PIDs (M-PID, NS-PID and S-PID)?

The M-PID is the merchant’s own code (usually your SKU). The NS-PID is the manufacturer’s or supplier’s unique product code. The S-PID is a standardised barcode number such as a GTIN, EAN or UPC. The M-PID and NS-PID are mandatory; the S-PID is added where the product carries one.

Do B2B shipments need PIDs?

No. Low-value imports to VAT-registered business recipients are exempt from the PID requirement. The rule targets B2C distance sales of imported goods; wholesale imports to a registered EU business clear on the standard commercial track.

What happens if a shipment has no PID after 1 November 2026?

The declaration is incomplete, so the shipment can be held or delayed at the border, and missing or inconsistent identifiers can lead to brokerage friction, penalties, or a refused parcel returned at the sender’s cost.

Is the PID the same as the €3 flat duty?

No. The €3 flat duty is a charge introduced on 1 July 2026 when the €150 exemption was removed; the PID is a data requirement that starts on 1 November 2026. A parcel can owe the duty and still be stopped for a missing identifier, so treat them as two separate tracks.

If your EU-bound shipments include a B2C leg, the safest move is to map your catalogue to the three PID fields during the voluntary window and test a few live declarations before November. We can review your lanes and file the data with the declaration so nothing waits at the border: request a quote or run your route through the rate calculator to start.

By the Sea Gate Logistics Editorial Team. Prepared from public EU customs guidance current at July 2026; rules and carrier procedures may change, so confirm specifics with your customs broker or the EU Taxation & Customs Union before filing.