IOSS after de minimis is now a half-answer to the import problem, not the whole one. The Import One-Stop Shop still does its job: a non-EU seller charges import VAT at checkout, files one monthly return, and the buyer pays nothing extra on VAT at the door. What changed on 1 July 2026 is everything IOSS was never built to handle. The EU removed its €150 customs-duty exemption and replaced it with a temporary flat duty of €3 per item, and that duty rides a separate customs track IOSS does not touch (EU Taxation & Customs Union). So a parcel with VAT fully prepaid can still be stopped for duty, held for missing data, or surcharged by the courier. IOSS covers roughly 93% of the low-value e-commerce parcels crossing into the EU (European Commission), which means this gap now sits under almost every cross-border order. This guide explains why prepaid VAT stopped guaranteeing a clean delivery, and what to do about it.

Key takeaways

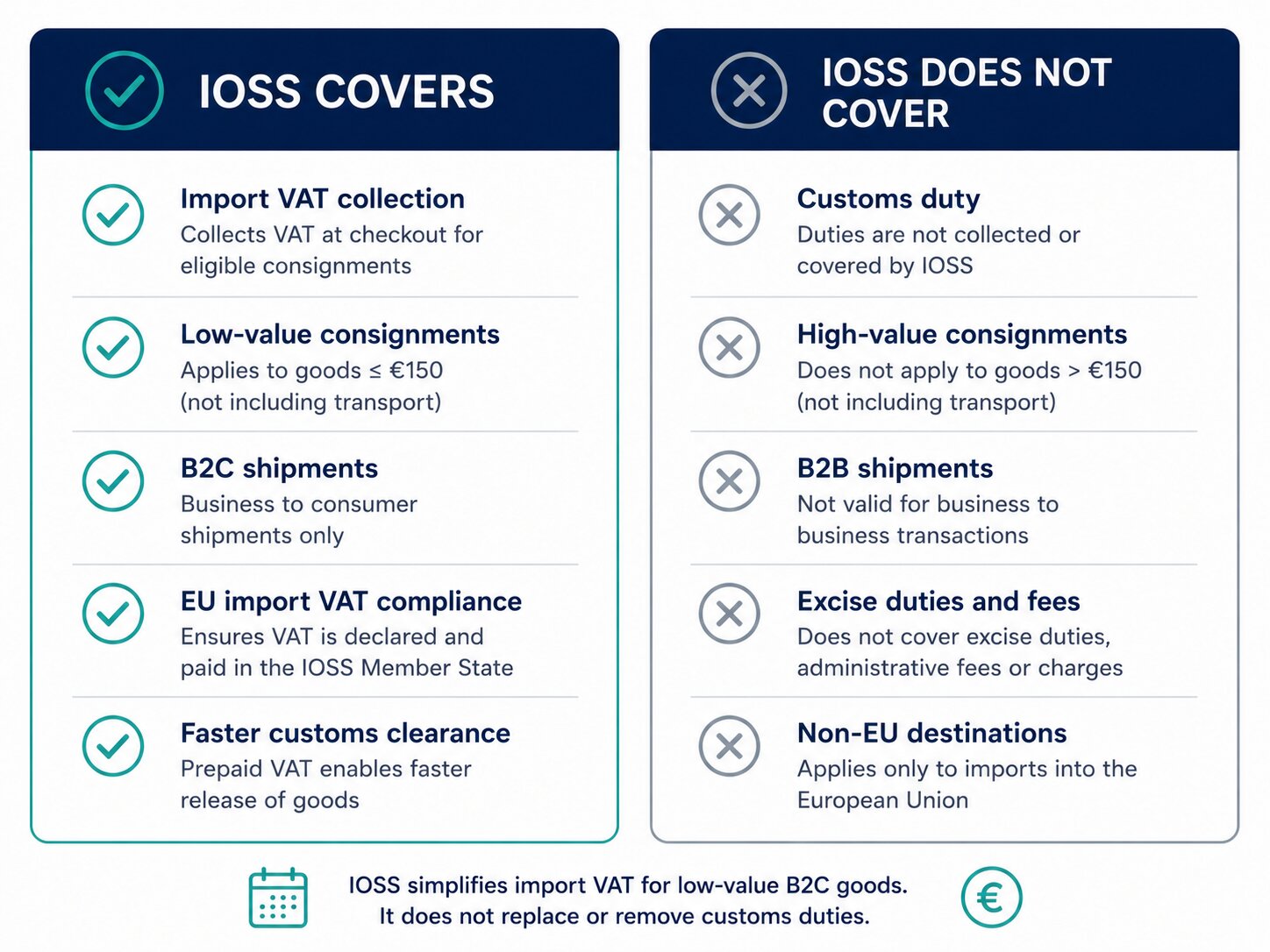

- IOSS is a VAT rail, not a customs pass. It collects and remits import VAT. It does not declare or clear the new €3 customs duty, which is assessed separately at the border (Avalara).

- The €3 duty applies even when you use IOSS. From 1 July 2026 it lands on qualifying consignments up to €150 regardless of VAT scheme. One bright side: no VAT is charged on the €3 duty itself for IOSS shipments (Global VAT Compliance).

- Prepayment only works if the IOSS number reaches customs. If it is not passed to the carrier and entered in the declaration, customs charges VAT again, causing double VAT, delays, and refused parcels (iCustoms).

- The €150 ceiling is on a countdown. From 1 July 2028 the EU Customs Data Hub goes live, normal product duties apply to all values, and the €150 IOSS threshold is withdrawn (vatcalc).

Scope and audience: this explains what IOSS does and does not cover after the EU’s de minimis reform, written for SME importers, non-EU e-commerce sellers, and the EU buyers receiving their goods. It focuses on how IOSS VAT prepayment interacts with the new customs-duty rules from 1 July 2026 onward. It is not tax or legal advice, and it does not cover the separate US $800 de minimis change except as context.

On this page

- The short answer

- What IOSS actually does

- What “after de minimis” changes

- Why prepaid VAT no longer means smooth delivery

- What IOSS covers vs what it doesn’t

- Worked example: a €140 parcel

- What to do about it

- FAQ

IOSS after de minimis: the short answer

VAT prepayment through IOSS still spares your buyer the import-VAT bill, but it no longer clears the parcel end to end. IOSS was only ever a VAT mechanism, and the new €3 customs duty is a separate charge collected at the border (Avalara). Before 1 July 2026, a sub-€150 parcel owed no customs duty at all, so once VAT was prepaid there was genuinely nothing left to settle. That is the world IOSS was designed for, and it is the world that just ended.

The distinction to hold onto: IOSS pays the VAT, not the duty, and after de minimis there is now a duty to pay. Everything else in this guide follows from that one split. A parcel can be VAT-perfect and still get stopped, because clearance now depends on data and duty that live outside the IOSS system.

What IOSS actually does (and where €150 comes from)

The Import One-Stop Shop is the EU’s single-registration route for collecting import VAT on business-to-consumer goods shipped from outside the union. Instead of the buyer being billed VAT on arrival, the seller charges it at checkout, then reports and remits it through one monthly IOSS return covering every EU country (EU Taxation & Customs Union). One registration, one return, VAT settled up front.

That convenience has always had a hard boundary: an intrinsic value of €150 per consignment. Intrinsic value means the price of the goods themselves, not the shipping, insurance, or other charges, as long as those appear separately on the invoice (Cross Border VAT). Cross that line and the consignment falls outside IOSS and into standard import procedures. The €150 figure is not a duty threshold or a rounding convenience; it is the ceiling the whole scheme is built on.

When it works, IOSS is genuinely smooth. It is also widely trusted: in 2024, 92% of EU imports valued under €150 involved an IOSS-registered importer, and the scheme covers around 93% of cross-border e-commerce parcels entering the union (European Commission). The problem is not that IOSS is broken. The problem is that sellers came to treat “IOSS number on the parcel” as shorthand for “nothing can go wrong at customs,” and after de minimis that shorthand is false.

What “after de minimis” changes

De minimis was the customs-duty relief that let low-value parcels enter the EU duty-free. Removing it does not touch IOSS directly, but it removes the reason IOSS used to be sufficient. Here is the timeline that matters:

- 1 July 2021: the EU scraps its €22 import-VAT exemption. VAT becomes due from the first euro, and IOSS launches to collect it (EU Taxation & Customs Union).

- 13 November 2025: the EU Council votes to abolish the €150 customs-duty exemption (Avalara).

- 1 July 2026: the €150 duty exemption is replaced by a temporary flat customs duty of €3 per item, charged by tariff classification rather than quantity, with full declaration data required. Items sharing one HS code can group onto a single declaration line for one €3 charge (EU Taxation & Customs Union).

- 1 November 2026: Product Identifier (PID) data becomes mandatory (voluntary from 1 July), and a Union handling fee of about €2 per consignment is expected around the same window (Avalara; vatcalc).

- 1 July 2028: the flat €3 duty ends, the EU Customs Data Hub goes live, and normal product-specific duties apply to goods of any value. Critically, the €150 VAT threshold IOSS depends on is withdrawn, so VAT and customs are collected at checkout regardless of value (vatcalc).

The scale behind these dates explains the urgency. Around 4.6 billion low-value items entered the EU in 2024, roughly 12 million parcels a day and about double the year before, with 91% originating in China and the Council pointing to estimates that up to 65% of small parcels are undervalued to dodge duty (European Commission; European Parliament). A regime that waved those through on trust was always going to close.

Why prepaid VAT no longer means smooth delivery

Here is the part generic “de minimis is ending” coverage skips. It reports the €3 duty and IOSS as two separate news items, and never connects them to the seller’s actual question: I already prepay VAT, so why is my parcel stuck? VAT prepayment is now necessary but not sufficient. Four distinct gaps can stop a fully VAT-paid parcel, and it helps to name them.

1. The duty gap. IOSS clears VAT and nothing else. The €3 per-item duty is a customs charge collected at the border, on a separate track, and it applies to qualifying low-value consignments regardless of VAT scheme, IOSS included (Global VAT Compliance). Your VAT can be flawless and the parcel still owes duty IOSS never declared. There is one small mercy: for IOSS shipments, no VAT is charged on top of the €3 duty itself (vatcalc).

2. The €150 ceiling. IOSS applies only up to €150 intrinsic value. Add a second item, or let a buyer bump the order, and a €140 basket becomes a €165 consignment that drops out of IOSS entirely and into a full standard declaration, carrying real product duty, more paperwork, and carrier fees the checkout price never accounted for. The ceiling is silent. Nothing warns you the moment an order tips over it.

3. The transmission gap. Prepaying VAT and proving you prepaid it are two different things. IOSS only works if the seller’s IOSS number is passed to the carrier and entered in the customs declaration (typically box 44). If it is missing, or fails validation in a full H1 declaration, customs cannot see that VAT was paid and charges it again, producing double VAT, rejected declarations, and delivery delays (iCustoms; EAS). Post-reform, every parcel carries more mandatory data, which means more points where that link can break. Marketplace sellers already report issued IOSS numbers failing at clearance and customers billed twice.

4. The H7 tradeoff. Using IOSS routes the parcel through the simplified H7 customs dataset. But goods that qualify for a preferential duty rate under a trade agreement can only claim it on a standard H1 declaration where VAT was not collected via IOSS (Global VAT Compliance). In other words, the simplest VAT path can quietly forfeit a lower duty rate the goods were entitled to. For most low-value consumer parcels this is marginal; for the right product it is real money.

Would you rather absorb a €3 duty and a €2 fee quietly at your end, or let a courier surprise your customer with them at the door? That is the question these four gaps really pose, and prepaid VAT alone does not answer it.

What IOSS covers vs what it doesn’t

One view of the split, after 1 July 2026:

| Obligation | Covered by IOSS? | Who handles it |

|---|---|---|

| Import VAT (≤ €150 consignment) | Yes, charged at checkout, filed monthly | Seller, via IOSS return |

| €3 flat customs duty (per item) | No, separate border charge | Carrier / customs broker at import |

| Full customs declaration + PID data | No | Carrier / broker |

| ~€2 Union handling fee | No | Carrier, billed at clearance |

| Consignments over €150 | No, outside IOSS entirely | Standard import (duty + VAT at border) |

| Preferential duty rate (trade agreement) | No, needs H1 and non-IOSS VAT | Broker on a full declaration |

The pattern is plain: IOSS owns one column of the import bill, and after de minimis that column is no longer the whole invoice.

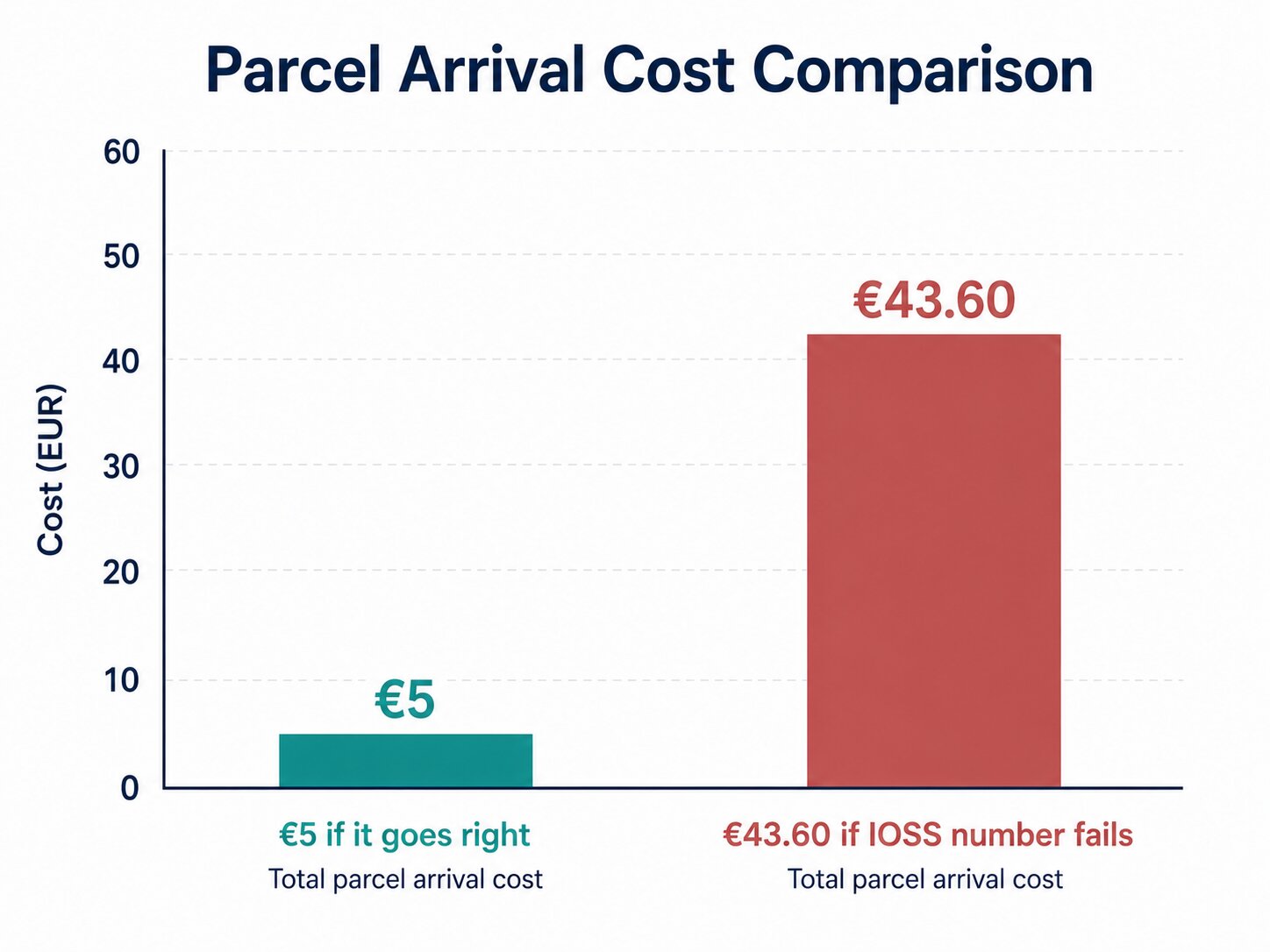

Worked example: a €140 parcel that ships fine, until it doesn’t

Numbers make the gap concrete. Take a €140 consignment of consumer goods shipped B2C from outside the EU to Germany after 1 July 2026, sold with IOSS. Every figure below is Estimated, built from published EU rates and typical broker charges to show the mechanism, not a quote.

| Cost line (€140 IOSS parcel → Germany) | If it goes right | If IOSS number doesn’t transmit |

|---|---|---|

| Import VAT (19%, prepaid at checkout) | €26.60 (already paid) | €26.60 charged again at the door |

| €3 flat customs duty (1 item, 1 HS code) | €3 | €3 |

| ~€2 Union handling fee | €2 | €2 |

| Courier VAT-disbursement/admin fee | €0 | ~€12 |

| Buyer pays on arrival (Estimated) | €5 | ≈ €43.60 |

In the good column, the buyer still owes €5 they may not have expected. Small, but no longer the zero IOSS implied. In the bad column, a broken IOSS link turns a prepaid parcel into a €43.60 collect-on-delivery shock, most of it double-charged VAT the seller already remitted. That is how a “VAT is handled” order becomes a chargeback and a one-star review.

Now scale it. A seller shipping 40 small orders a week is not fighting one €3 duty; it is 40 separate per-item duties, 40 handling fees, and 40 chances for a number to fail transmission. On EU and Balkan lanes we increasingly consolidate those into one properly declared shipment, so the duty and clearance are handled once, cleanly, instead of stacking parcel by parcel. [case study placeholder: a real Sea Gate consolidation setup and its landed-cost breakdown will be inserted here.]

What to do about it: a short decision framework

Walk these four questions against your own flow before you assume IOSS has you covered.

- Is every consignment genuinely under €150 intrinsic value? If orders regularly tip over, through bundles or multi-item baskets, plan for full declarations, because those parcels leave IOSS the moment they cross the line.

- Does your IOSS number reliably reach the carrier and the declaration? Confirm with your carrier or broker exactly which field carries it and how failures are flagged. This single link is where most double-VAT cases start.

- Who absorbs the €3 duty and ~€2 fee, you or the customer at the door? Baking them into your landed price protects the delivery experience; leaving them for the courier to collect invites refusals.

- Would consolidation beat per-parcel shipping? High order volumes of small items pay the €3-and-fee stack again on every parcel. Grouping them into one declared shipment, or moving to a DDP arrangement where the goods arrive fully cleared, can be cheaper and calmer than IOSS alone.

If the Incoterm side of this is unfamiliar, our companion guide on DDP vs DAP after de minimis covers who becomes the importer of record. For the consolidation route, our consolidated cargo service is built for exactly the low-volume, many-orders shipper this reform hits hardest. And if you would rather have someone map the whole landed cost before 2028 changes it again, talk to us; we do this on EU and Balkan lanes every week.

FAQ

Does IOSS cover customs duty?

No. IOSS collects and remits import VAT only. The €3 flat customs duty introduced on 1 July 2026 is a separate charge assessed at the border, and it is not declared or cleared through IOSS (Avalara).

Do I still need IOSS now that de minimis is ending?

Yes, for B2C goods under €150. IOSS still spares your buyer the import-VAT bill at delivery and keeps clearance faster. It simply no longer settles the full import cost, because customs duty now applies on top.

Why was VAT charged twice on a parcel that used IOSS?

Almost always because the IOSS number did not reach customs. It was not passed to the carrier, or it failed validation in the declaration. Customs then cannot see the prepaid VAT and charges it again, plus a courier admin fee (iCustoms; EAS).

Does the €3 duty apply to IOSS shipments?

Yes. The €3 per-item duty applies to qualifying low-value consignments regardless of VAT scheme, IOSS included. The only relief is that no VAT is charged on the €3 duty itself for IOSS transactions (Global VAT Compliance).

What happens to IOSS and the €150 threshold in 2028?

From 1 July 2028 the EU Customs Data Hub goes live, the temporary €3 duty ends, normal product duties apply to all values, and the €150 IOSS threshold is withdrawn. VAT and customs then get collected at checkout regardless of consignment value (vatcalc).

Can consolidating small orders reduce these charges?

Often, yes. Shipping many small parcels means paying the €3 duty and handling fee on each one. Grouping orders into a single, properly declared shipment through a forwarder handles duty and clearance once rather than repeatedly, which is worth modelling if you send steady volumes of low-value goods.

By the Sea Gate Logistics Editorial Team