DDP vs DAP shipping from Turkey now decides one thing above all: who pays the EU import bill once the de minimis loophole is gone. Under DDP (Delivered Duty Paid), the Turkish seller clears customs and pays the import duty, the import VAT, and the handling fees, so the EU buyer receives a fully landed parcel with nothing to settle. Under DAP (Delivered at Place), the buyer is the importer of record and pays those charges on arrival. Until recently a low-value parcel from Turkey often slipped through with little or no duty and light paperwork. From 1 July 2026 the EU removes its €150 customs-duty exemption and replaces it with a flat €3 duty per item, and every parcel needs a full declaration (EU Taxation & Customs Union). That makes the Incoterm you pick a real money-and-experience decision, not a line of boilerplate. This guide compares the two for the Turkey-to-EU lane and adds the one detail most articles skip: the EU-Türkiye Customs Union, which keeps duty on many Turkish goods at zero anyway.

Key takeaways

- DDP = seller pays, DAP = buyer pays. The choice does not change the total EU import bill. It changes who fronts it and who gets surprised at the door.

- De minimis is ending, so the bill is no longer near-zero. From 1 July 2026 a flat €3 duty per item replaces the EU’s €150 duty exemption, with a ~€2 handling fee following by 1 November 2026 (Avalara; EU Taxation & Customs Union).

- Turkey is a special case. Under the EU-Türkiye Customs Union, industrial goods in free circulation move duty-free with an A.TR certificate. For those goods the real change is paperwork and VAT, not the headline duty.

- Import VAT never went away. The EU scrapped its €22 VAT exemption back in 2021, so VAT has been due from the first euro since then (EU Taxation & Customs Union). DDP means the Turkish seller carries that 19-27% too.

Scope and audience: this compares the DDP and DAP Incoterms® 2020 rules for shipping from Turkey into the EU, for SME exporters, e-commerce sellers, and the EU importers buying from them. It focuses on customs duty, import VAT, and the fees that changed with de minimis. It is not legal or tax advice, and it does not cover the US $800 rule except as timeline context, or Turkey’s separate agricultural and steel arrangements.

On this page

- The short answer

- What “after de minimis” actually means

- DDP vs DAP: the core difference

- The Turkey exception: the EU Customs Union and A.TR

- What actually changes for Turkey

- DDP vs DAP side by side

- Worked example: a €120 Turkish parcel

- When to choose DDP vs DAP

- Questions to ask your forwarder

- Which should you pick?

- FAQ

DDP vs DAP from Turkey: the short answer

Pick DDP when you want the EU buyer to pay nothing on arrival, and DAP when the buyer is set up to clear customs and would rather control the import themselves. That is the whole distinction: DDP puts the Turkish exporter in the importer-of-record seat, paying EU duty, import VAT, and clearance; DAP hands that seat, and the bill, to the buyer at the destination (ICC Academy). Neither term makes the charges disappear. They only decide whose account the invoice lands on.

De minimis is what turned this from a formality into a decision. While low-value parcels cleared duty-free and informally, the difference between DDP and DAP was often a few euros of VAT. From 1 July 2026 the EU’s €150 duty exemption is replaced by a flat €3 duty per item, and full customs data becomes mandatory for every shipment (EU Taxation & Customs Union). Now the term you write on the invoice governs who absorbs a real, recurring per-parcel cost, and who has to answer for it when a customer complains about a surprise fee.

What “after de minimis” actually means

Two separate de minimis regimes changed within a year, and it helps to keep them apart. The United States ended its long-standing $800 duty-free threshold first: Executive Order 14324, signed 30 July 2025, suspended duty-free de minimis treatment for all countries from 29 August 2025, after China’s own exemption had already ended on 2 May 2025 (White & Case; EY). That is the change that filled the headlines, but it governs parcels entering the US, not the EU.

For a Turkish exporter, the EU timeline is the one that bites:

- Since 1 July 2021: the EU’s €22 import-VAT exemption is gone. Import VAT is due on every commercial parcel from the first euro, collected through IOSS or at the border (EU Taxation & Customs Union).

- 13 November 2025: the EU Council votes to scrap the €150 customs-duty exemption (Avalara).

- 1 July 2026: the €150 duty exemption is replaced by a temporary flat customs duty of €3 per item, and full declaration data is required.

- By 1 November 2026: an EU-wide handling fee of about €2 per HS code applies, and Product Identifier (PID) data becomes mandatory (Avalara).

- 1 July 2028: the flat €3 duty ends and normal, product-specific duties apply once the EU Customs Data Hub is live (EU Taxation & Customs Union).

The scale explains the urgency. Around 4.6 billion low-value consignments entered the EU in 2024, roughly 12 million parcels a day and about double the year before (European Commission). A system that waves those through on trust is exactly what Brussels set out to close.

DDP vs DAP: the core difference

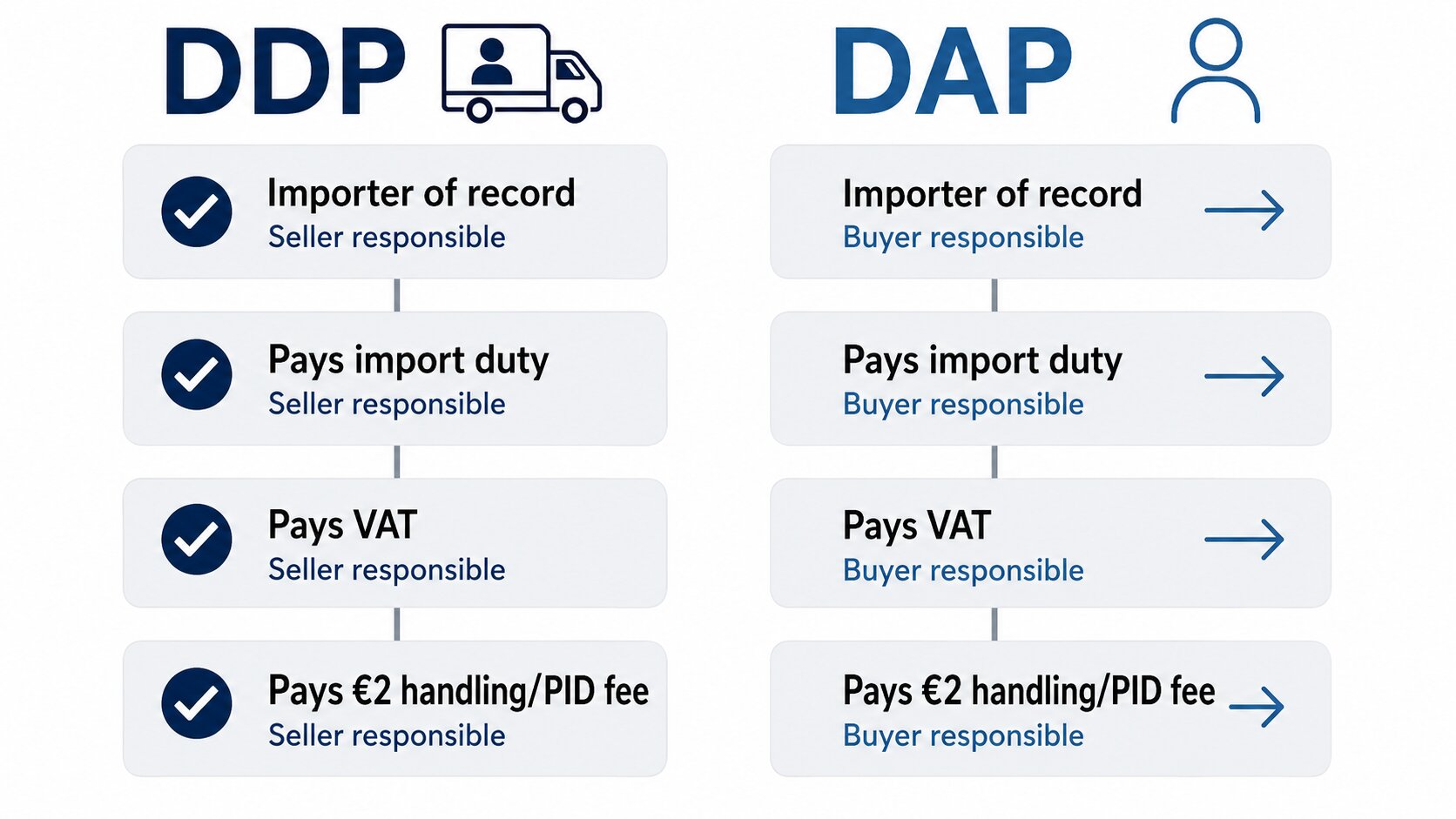

Both terms are Incoterms® 2020 delivery rules, and both put the seller in charge of transport all the way to the buyer’s address. They split on one clause: who acts as the importer of record in the destination country. That single difference cascades into who pays, who files, and who carries the risk of a mistake.

DAP (Delivered at Place) stops the seller’s obligations at the point the goods are ready for unloading at the named destination. The buyer clears import customs, pays the import duty and import VAT, and handles any licences (ICC Academy). The seller never touches the EU tax system.

DDP (Delivered Duty Paid) is the maximum-obligation term for a seller. The Turkish exporter delivers the goods cleared for import, having paid the duty, the VAT, and every customs formality at destination (Trade Finance Global). In a VAT territory that VAT alone runs 19-27% of the goods value depending on the country (Germany 19%, Netherlands 21%), so DDP is a serious commitment, not a courtesy.

One practical trap sits inside DDP. To pay import VAT in the EU, the Turkish seller usually needs an EU VAT registration and an EORI number, or a customs representative willing to act for them. Promise a buyer DDP without that groundwork and the parcel stalls at the border, which is the opposite of the smooth experience DDP is meant to deliver.

The Turkey exception: the EU Customs Union and A.TR

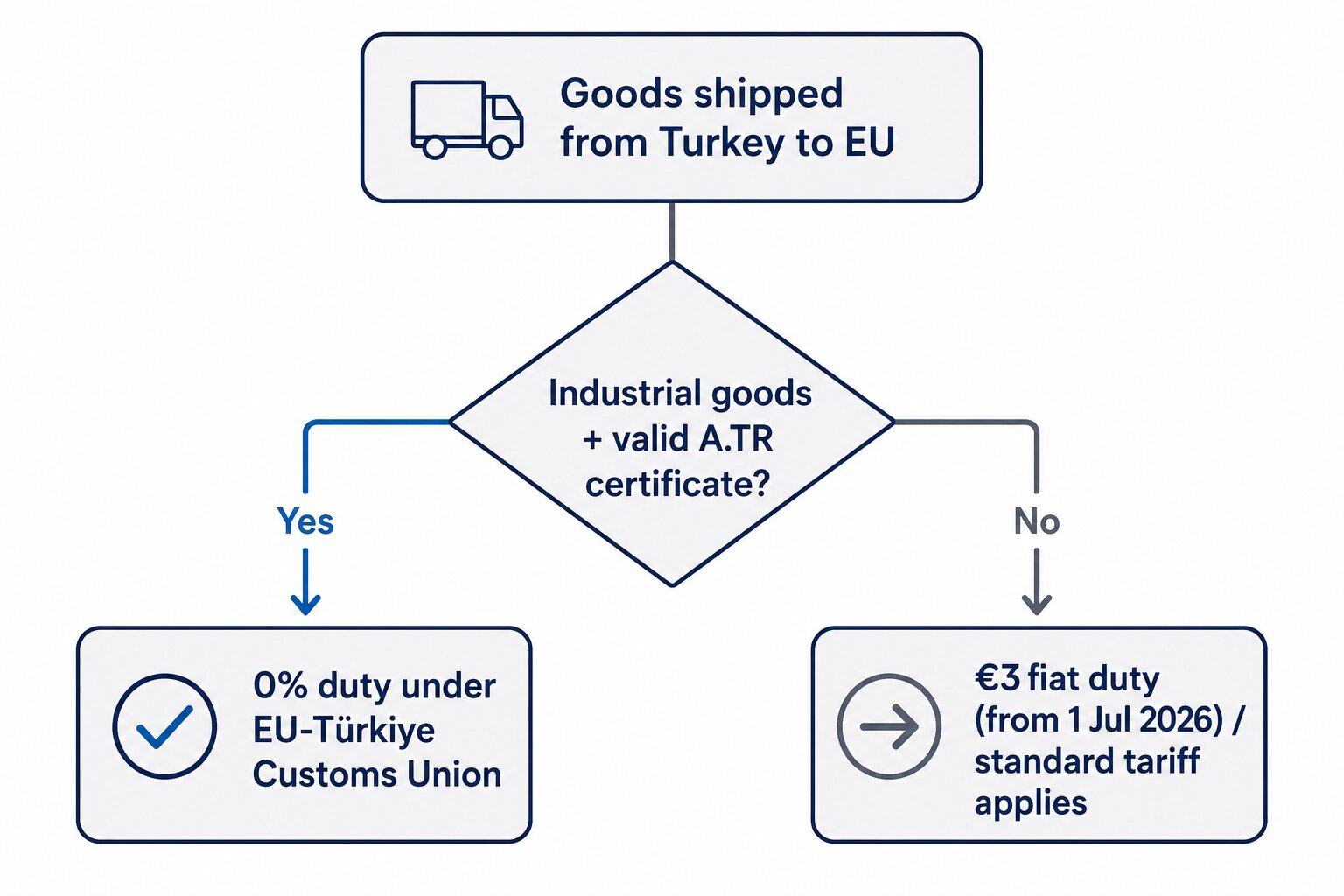

Here is the detail that reshapes the whole comparison for Turkey, and that generic “de minimis is ending” coverage almost always misses. Turkey and the EU have shared a Customs Union since 1995. Industrial products, and the industrial component of processed agricultural goods, that are in free circulation move between Turkey and the EU free of customs duty (EU Taxation & Customs Union). The duty-free status is claimed with an A.TR movement certificate, a document that certifies free circulation rather than origin (Access2Markets).

So what does the €3 flat duty mean for a Turkish sofa cover, a pair of jeans, or an auto part? If the goods qualify as industrial and travel with a valid A.TR, the customs duty was already zero, and it stays zero. The de minimis change does not suddenly impose a tariff that the Customs Union already removed. This is the structural reason a parcel from Istanbul is not in the same position as an identical parcel from Shenzhen.

Two limits keep this from being a free pass. First, the A.TR clears duty only; it does nothing for import VAT, which is still due at the destination rate on entry (EU Taxation & Customs Union). Second, the Customs Union does not cover everything: basic agricultural products and coal and steel (ECSC) goods sit outside it under separate arrangements, so a shipment of Turkish produce follows different rules than a shipment of Turkish textiles. Know which category your goods fall into before you price the term.

What actually changes for Turkey after de minimis

Strip away the headline and the real shift for a compliant Turkish exporter is administrative, not tariff-driven. The customs duty on qualifying industrial goods stays at zero under the Customs Union; what arrives is a stack of new obligations on every single parcel that used to travel informally:

- A full customs declaration per parcel. The informal, data-light clearance that low-value goods enjoyed is over from 1 July 2026 (EU Taxation & Customs Union).

- A valid A.TR to keep duty at zero. Without the certificate (or a supplier’s declaration where relevant), a parcel can lose its Customs Union treatment and face the flat €3 duty or standard rates.

- Accurate HS codes and PID data. Product Identifier data becomes mandatory by 1 November 2026; a wrong or missing code invites delay and reassessment (Avalara).

- The ~€2 EU handling fee per HS code. Small per parcel, but it scales fast across an e-commerce catalogue moving thousands of orders.

- Import VAT, collected reliably. VAT has been due since 2021, but tighter data means fewer parcels slip through unassessed. On a €120 order at German rates that is €22.80, dwarfing any duty question.

Turkey’s exposure here is concentrated. Türkiye’s e-commerce exports are projected near $8 billion, with textiles and ready-to-wear the most affected category, which is why Turkish trade bodies have pressed the EU for an exemption (Daily Sabah). For an SME seller, the cost is less the duty and more the compliance overhead per shipment, and that is precisely the burden DDP shifts onto the exporter and DAP leaves with the buyer.

DDP vs DAP side by side

Here is the comparison in one view, framed for a Turkey-to-EU shipment after de minimis. Treat the VAT and fee figures as the pattern; the exact numbers move with country and product.

| Factor | DDP (Delivered Duty Paid) | DAP (Delivered at Place) |

|---|---|---|

| Importer of record | The Turkish seller | The EU buyer |

| Pays EU customs duty | Seller (€0 with valid A.TR on industrial goods; else €3 flat, then standard from 2028) | Buyer (same duty logic) |

| Pays import VAT (19-27%) | Seller | Buyer |

| Pays ~€2 handling fee | Seller | Buyer |

| Needs EU VAT/EORI or a representative | Yes, the seller does | No, the buyer already has standing |

| Buyer experience | Nothing to pay on arrival | Pay-on-delivery, possible surprise fee |

| Best for | B2C e-commerce, buyers who want it landed | B2B buyers set up to import |

The row that matters most is the last-but-one. After de minimis, a DAP parcel arriving with an unexpected duty-plus-VAT-plus-fee invoice is the single fastest way to a refused delivery or a one-star review. DDP removes that shock by moving it upstream, into the seller’s pricing.

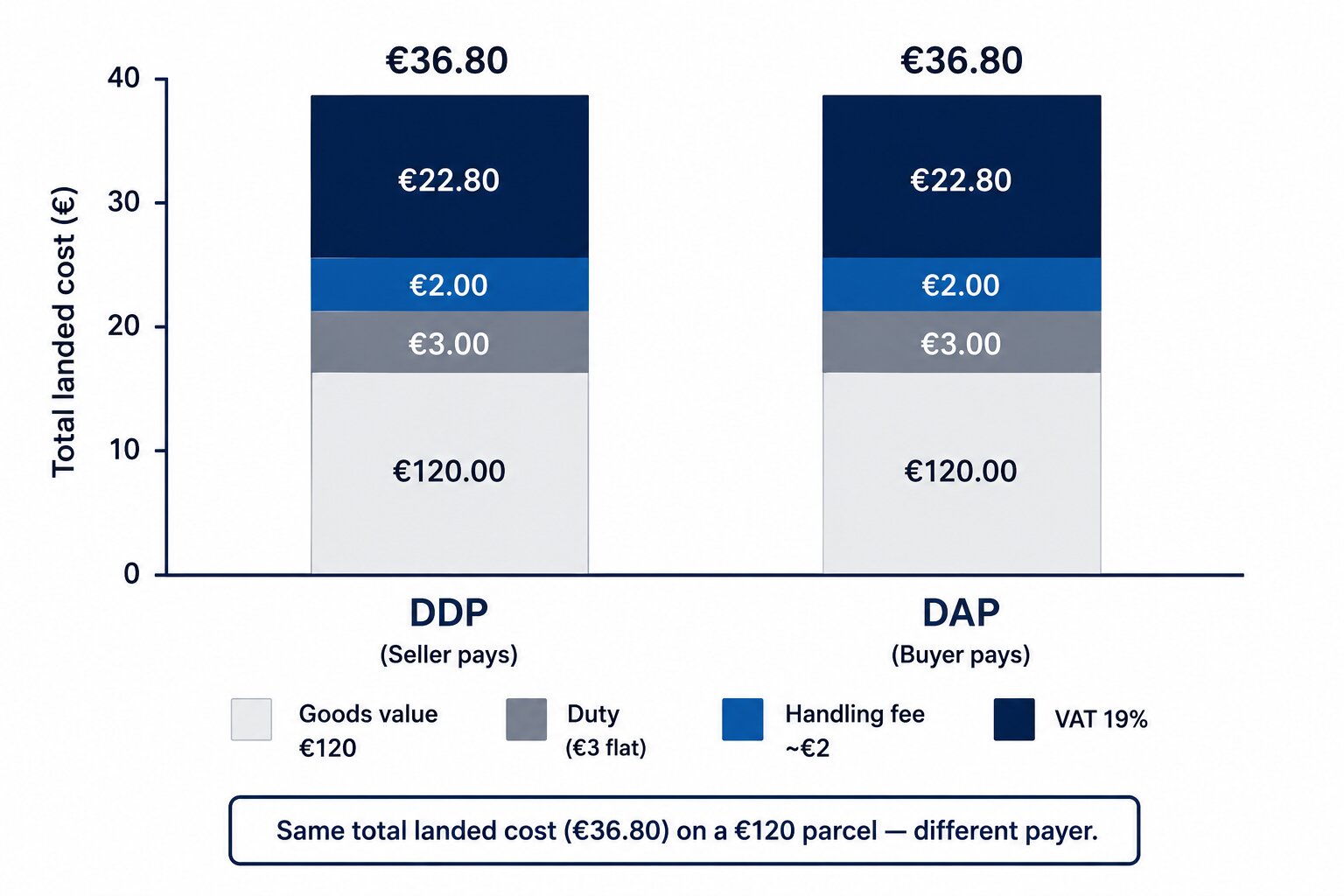

Worked example: a €120 Turkish parcel, DDP vs DAP

This is where the “who pays” abstraction becomes a number. Take a €120 consignment of Turkish ready-to-wear (an industrial good under the Customs Union) shipped to a consumer in Germany after 1 July 2026. Every figure below is Estimated — illustrative values built from published EU rates and typical broker charges to show the mechanism, not a live quote. Your real numbers move with product, country, and carrier.

| Cost line (€120 parcel, Turkey → Germany) | DDP (seller pays) | DAP (buyer pays) |

|---|---|---|

| Customs duty (valid A.TR, industrial good) | €0 | €0 |

| EU handling fee (~€2 per HS code) | €2 | €2 |

| Import VAT (Germany, 19%) | €22.80 | €22.80 |

| Broker / clearance fee | €12 | €12 |

| Total added at the border (Estimated) | ≈ €36.80 | ≈ €36.80 |

| Who is billed | Seller (baked into the price) | Buyer (invoiced on arrival) |

Read the totals, then read the last row. The all-in cost is identical either way, about €36.80 on a €120 order. DDP and DAP do not change that total by a cent. What they change is who fronts the roughly €37 and who feels ambushed by it. Before de minimis ended, that same parcel might have cleared informally with little more than the VAT to worry about, so the choice of term barely registered. Now the €37 is structural, on every parcel, which is exactly why the Incoterm has graduated from paperwork to strategy.

On Turkey-to-EU lanes we usually steer SME e-commerce sellers toward DDP for consumer orders, because a German or Dutch buyer who has to answer the door to a courier demanding VAT tends not to order twice. The honest caveat: DDP only works once the seller has the EU VAT registration and EORI (or a customs representative) in place, and if the goods are agricultural or steel rather than industrial, the zero-duty assumption in the table above no longer holds. [case study placeholder — a real Sea Gate Turkey→EU DDP setup and its landed-cost breakdown will be inserted here.]

When to choose DDP vs DAP: a decision framework

Walk these five questions in order against your own shipment. The first two usually settle it.

- Who is the buyer? Selling B2C to consumers → lean DDP, because shoppers expect a landed price and will not clear customs. Selling B2B to a company with its own EORI and broker → DAP is often cleaner.

- Are you set up to be the EU importer? DDP needs an EU VAT registration and EORI, or a customs representative acting for you. Without that groundwork, a DDP promise just stalls parcels at the border.

- What are the goods? Industrial goods with a valid A.TR clear duty-free, which makes DDP cheaper to offer than the headlines suggest. Agricultural or steel goods sit outside the Customs Union, so price the real duty before committing.

- How price-sensitive is the buyer relationship? DDP lets you quote one clean landed price and win on certainty. DAP lets you quote a lower headline price, as long as the buyer genuinely understands they pay duty and VAT on arrival.

- How many parcels, how often? High-volume e-commerce flows justify the one-time cost of EU VAT/EORI setup for DDP. A one-off B2B pallet rarely does; DAP avoids the overhead.

Choose DDP if: you sell to EU consumers, you can register for EU VAT (or appoint a representative), and you want zero surprises at the door. Choose DAP if: your buyer is a business ready to import, you would rather not carry EU tax obligations, and both sides accept the arrival invoice. In between, price both and let the total landed cost and the buyer experience decide together.

Questions to ask your forwarder before you book

A forwarder who knows the Turkey-EU lane will answer all five without hedging:

- Can you handle DDP clearance for me, and do I need my own EU VAT and EORI? You want to know whether they can act as, or arrange, your customs representative.

- Will my goods qualify for A.TR duty-free treatment, and can you issue the certificate? This is the difference between €0 and standard duty on industrial goods.

- What is the all-in landed cost per parcel, including VAT, the ~€2 handling fee, and clearance? Insist on the total to the door, not just freight.

- How will you supply the HS codes and PID data the new rules require? Missing data from 1 November 2026 means delay and reassessment.

- For DAP, how will the buyer be billed at destination, and are they briefed? A buyer who understands the arrival invoice does not refuse the parcel.

DDP vs DAP from Turkey: which should you pick?

Back to the question we opened with. For a Turkish SME selling to EU consumers after de minimis, DDP is usually the right call, because the buyer expects a landed price and the Customs Union already keeps industrial-goods duty at zero, so the term costs you less to offer than a China-based seller would pay. For B2B sales to a buyer with their own import setup, DAP is the simpler, lighter contract, and it keeps EU tax obligations off your books. The one thing that is true under both terms: the de minimis change made the EU import bill real and recurring, so the choice is no longer cosmetic.

The practical next step, if you are weighing the two, is to price a specific parcel both ways — with the A.TR duty treatment, the destination VAT, and the new fees all in — so the decision rests on your real numbers. Our road and consolidated freight on the Turkey corridor and our customs and forwarding team are set up to quote DDP and DAP side by side and to sort the A.TR paperwork before your goods move.

FAQ

What is the difference between DDP and DAP when shipping from Turkey?

Under DDP (Delivered Duty Paid), the Turkish seller is the importer of record and pays the EU customs duty, import VAT, and clearance, so the buyer receives the parcel with nothing to pay. Under DAP (Delivered at Place), the EU buyer clears customs and pays those charges on arrival. The total cost is the same; the term only decides who pays and who files (ICC Academy).

How does the end of de minimis change DDP vs DAP from Turkey?

Before de minimis ended, low-value parcels often cleared duty-free and informally, so the term barely mattered. From 1 July 2026 the EU replaces its €150 duty exemption with a flat €3 duty per item and requires a full declaration on every parcel (EU Taxation & Customs Union). That makes the per-parcel EU import bill real and recurring, so the choice of DDP or DAP now decides who absorbs a genuine cost.

Do Turkish goods still pay EU customs duty after de minimis?

Often not. Under the EU-Türkiye Customs Union, industrial goods in free circulation move duty-free with a valid A.TR movement certificate, and that treatment is unchanged by the de minimis reform (Access2Markets). The A.TR removes duty only, not VAT, and it does not apply to agricultural or coal-and-steel goods, which follow separate rules.

Does DDP from Turkey include EU import VAT?

Yes. DDP means the seller pays all import charges at destination, including import VAT, which runs about 19-27% of the goods value depending on the country (Germany 19%, Netherlands 21%). To pay it, the Turkish seller normally needs an EU VAT registration and an EORI number, or a customs representative acting on their behalf.

Is DDP or DAP better for e-commerce sellers shipping from Turkey to the EU?

DDP is usually better for B2C e-commerce, because consumers expect a landed price and will refuse a parcel that arrives with a surprise duty-and-VAT invoice. DAP suits B2B buyers who are set up to import. Because the Customs Union keeps industrial-goods duty at zero, offering DDP from Turkey is cheaper than the general de minimis coverage implies.

What is an A.TR certificate and why does it matter now?

An A.TR movement certificate proves that goods are in free circulation within the EU-Türkiye Customs Union, which lets industrial goods enter the EU free of customs duty (EU Taxation & Customs Union). After de minimis, every parcel needs full customs data, so a valid A.TR is what keeps duty at zero rather than defaulting to the €3 flat rate or standard tariffs. It does not remove import VAT.