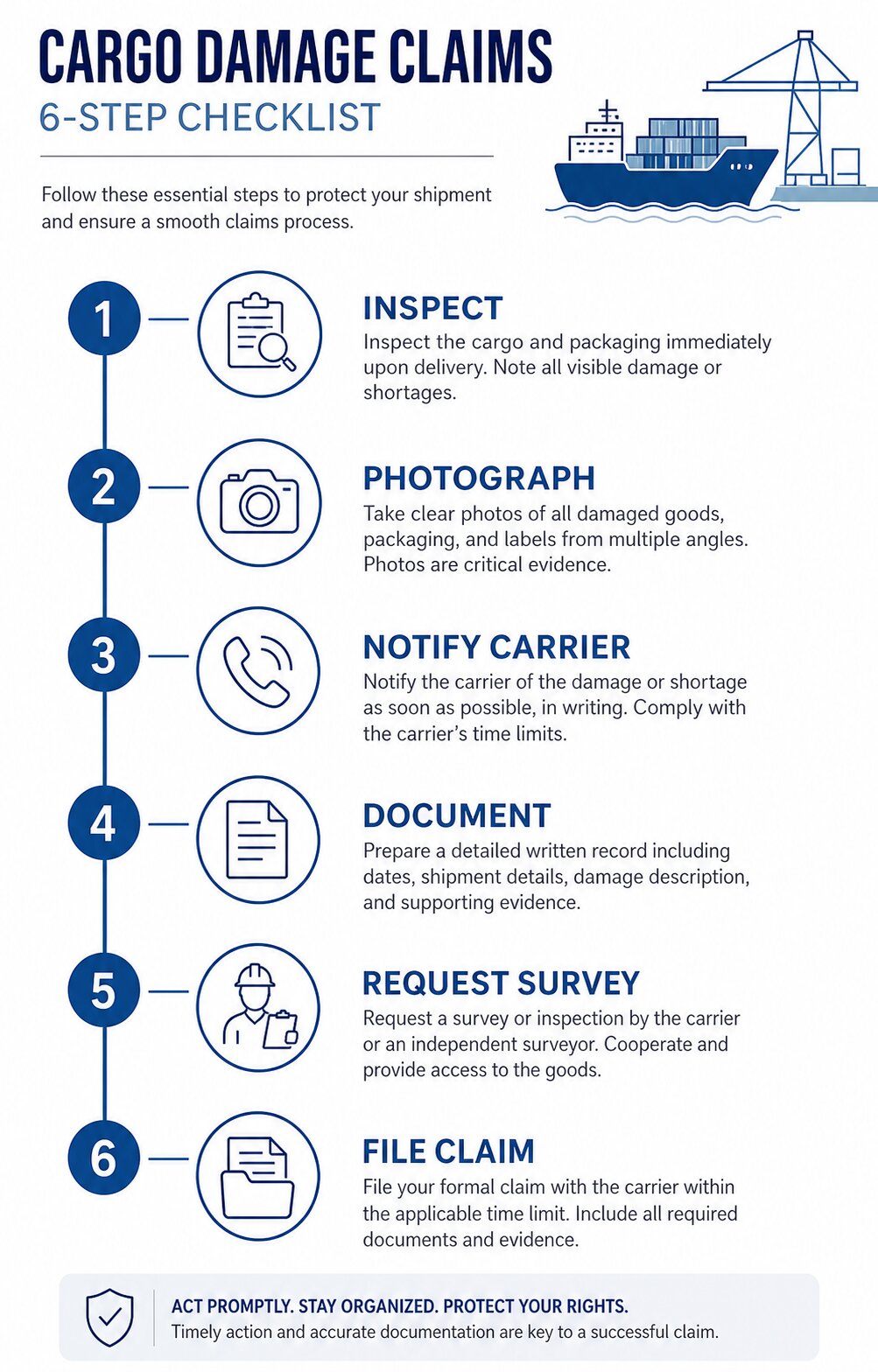

Knowing what to do if your cargo is lost or damaged starts before you sign anything: inspect the goods at delivery, and don’t sign a clean delivery receipt for a shipment you haven’t checked. Note the damage specifically on the proof of delivery (POD), CMR consignment note (the contract document for road freight), or air waybill, and back it up with dated photos. Notify the carrier and your insurer in writing within the deadline for your transport mode. Preserve the damaged goods and their packaging exactly as received, since the carrier may want to inspect them. Assemble your documents, including the invoice, packing list, and transport contract. Then file a written claim that names a specific amount. This guide covers international shipments under the CMR, Hague-Visby, and Montreal rules, written for SME importers and exporters moving FCL, LCL, or groupage. This is general information, not legal advice; conventions and limits vary by contract and jurisdiction.

Key takeaways

- Deadlines are short and mode-specific: sea concealed damage 3 days, road 7 days (CMR), air 14 days (Montreal).

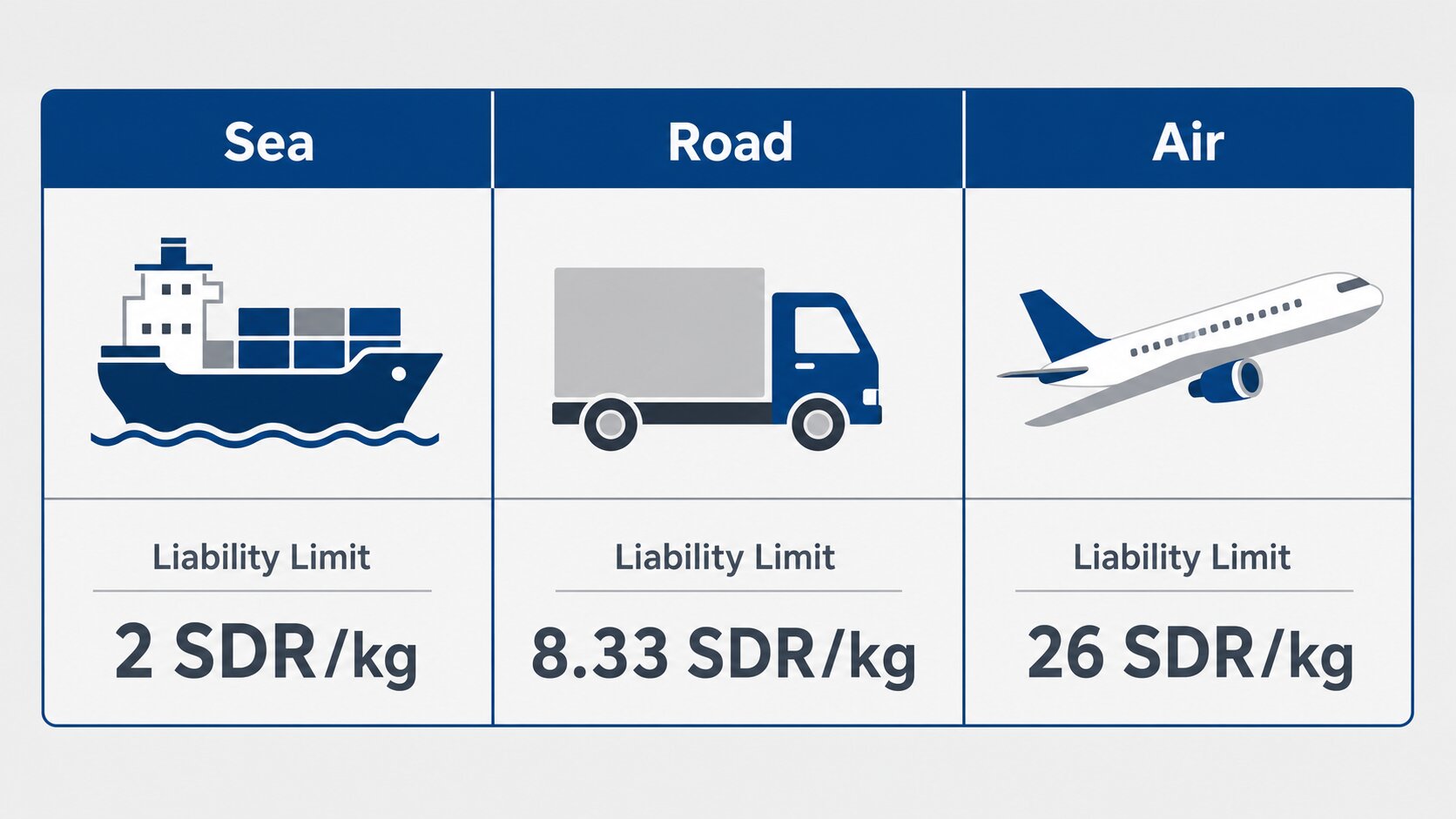

- Carrier liability is capped by convention (road CMR = 8.33 SDR per kg) and usually sits far below your cargo’s real value.

- Cargo insurance, not carrier liability, is what actually pays out your declared value.

- Under CMR Article 30, staying silent for 7 days means the goods are presumed delivered in good condition.

- The Incoterm you ship on decides who bears transit risk, and therefore who files the claim.

First 48 Hours: Your Action Checklist

Most carrier conventions give you only a few days to register visible damage, and a clean signature on delivery is treated as evidence the goods arrived intact. What you do on the dock decides whether a later claim survives.

- Inspect the cargo before you sign anything. Open the load, count the units, and check for crushing, wet marks, or broken seals while the driver waits.

- Note the damage specifically on the POD (proof of delivery) / CMR consignment note / air waybill. Write what you see, not “received”: for example, “2 cartons crushed, water-stained, outer wrap torn.” A vague signature closes the door on disputes.

- Photograph everything. Cartons, the pallet, seals, packaging, and each point of damage, with timestamps if your phone allows.

- Notify the carrier AND your insurer in writing immediately. A phone call is not a record; send an email the same day.

- Preserve the goods and all packaging. Keep the damaged units and every box, wrap, and pallet, because the carrier or an appointed surveyor may want to inspect them.

- Keep the original transport document (Bill of Lading, CMR note, or air waybill). It anchors the claim and proves who held the goods.

Would you really sign for cargo you haven’t opened? A note like “subject to inspection” is often treated as too vague to hold the carrier. Specific, written reservations (counts, conditions, exact wording) are what protect the claim weeks later when memories and goodwill have faded.

Who Is Liable for Damaged Freight? Carrier, Forwarder, or Insurer

The burden of proof sits with the claimant: to recover from a carrier, you must show the goods were tendered in good order and then lost or damaged while in the carrier’s “care, custody and control.” Three things have to be established:

- the goods were handed over in good condition (a clean Bill of Lading or CMR note with no damage notations);

- the loss or damage happened in transit, while the goods were in the carrier’s custody;

- the quantified value of the loss, backed by invoices or valuations.

Three actors can sit behind a damaged shipment. The carrier is the vessel operator, trucking company, or airline that physically moves the goods; it is liable while the cargo is in its custody, but its payout is capped by the governing convention. The freight forwarder arranges and books the carriage; it is liable for loss or damage mainly when it acts as the contracting carrier or is negligent, not automatically for every dented carton. The insurer pays the insured value under your cargo policy, then pursues the carrier itself. That recovery runs through subrogation (after paying you, the insurer steps into your shoes to chase the carrier for what it can collect).

Carrier liability is capped well below the real value of most cargo. The Hague-Visby Rules govern sea freight, the CMR Convention road, and the Montreal Convention 1999 air. Those caps are weight-based, not value-based. The gap they leave is quantified in the sections that follow.

Carrier Liability Limits by Convention (Sea, Road, Air)

The Special Drawing Right (SDR) is a reserve-currency unit defined by the International Monetary Fund and used to set transport liability caps. One SDR is worth roughly US$1.3 (Estimated, and it fluctuates, so check the live IMF rate). Each transport mode sits under a different convention, and each convention caps what the carrier owes per kilogram or per package.

| Mode | Convention & article | Carrier liability cap | Notes |

|---|---|---|---|

| Sea / ocean | Hague-Visby Rules | 2 SDR per kg, or 666.67 SDR per package/unit, whichever is higher | The higher of the two applies; how cargo is “packaged” can change the result |

| Road (international, Europe) | CMR Convention, Art. 23 | 8.33 SDR per kg of gross weight short or damaged | Carriage charges and duties refunded pro rata |

| Air | Montreal Convention 1999, Art. 22 | 26 SDR per kg | Raised from 22 SDR on 28 December 2024; reviewed every 5 years for inflation |

The air figure changed recently. According to the International Civil Aviation Organization, the Montreal cap rose to 26 SDR per kg on 28 December 2024, up from 22 SDR, so many guides and even some carrier contracts still quote the old number. Under the Hague-Visby Rules, the two sea calculations run in parallel and the higher result wins, which means a light, high-value package can sometimes claim more under the per-package figure than under the per-kg one. Per Article 23 of the CMR Convention, road carriage in Europe is capped at 8.33 SDR per kg of the weight actually short or damaged. The US works differently. Domestic road carriage there runs under the Carmack Amendment, not the CMR, with its own rules and deadlines.

Claim Time Limits by Mode: Don’t Miss the Deadline

A late notice can extinguish a claim that would otherwise have paid out in full. The deadlines below run from delivery, and they are short.

| Mode | Notice of apparent damage | Notice of concealed damage | Deadline to bring suit (limitation) |

|---|---|---|---|

| Sea (Hague-Visby) | At delivery, on the receipt | Within 3 days of delivery | 1 year from delivery |

| Road (CMR) | Reservation at the time of delivery | In writing within 7 days (excluding Sundays and public holidays) | 1 year (3 years for wilful misconduct), CMR Art. 32 |

| Air (Montreal) | Within 14 days of receipt | Within 14 days of receipt (21 days for delay) | 2 years to sue, Montreal Art. 31 |

The CMR adds a trap worth knowing. Under Article 30 of the CMR Convention, if the consignee accepts the goods without a written reservation within 7 days (excluding Sundays and public holidays) for non-apparent damage, the goods are presumed to have been received in the condition described in the consignment note. In plain terms, silence is treated as acceptance. Miss the window and the claim is effectively gone. US domestic road claims under the Carmack Amendment must be filed within 9 months, and the carrier then has 30 days to acknowledge and 120 days to resolve.

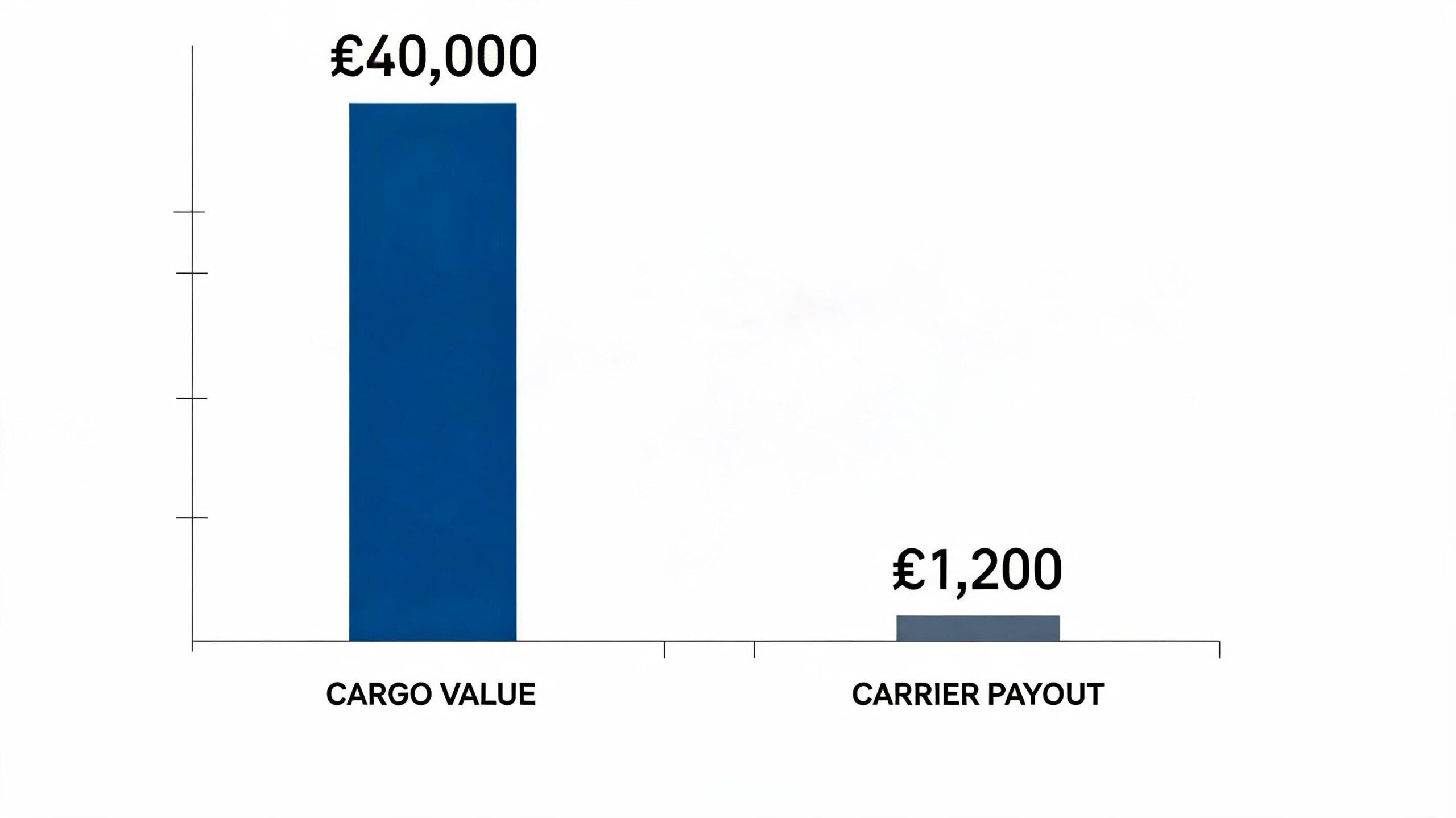

Why the Carrier Won’t Pay Full Value: A Worked Example

A convention cap and the real value of your cargo are rarely close. Take a 500 kg pallet of electronics worth €40,000 that is lost in transit, and run the cap calculation for two modes.

| Mode | Cap calculation | Approx. carrier payout vs €40,000 value |

|---|---|---|

| Sea (Hague-Visby, 2 SDR/kg) | 500 kg × 2 SDR = 1,000 SDR | ≈ €1,200–1,300 (Estimated), about 3% of value |

| Air (Montreal, 26 SDR/kg) | 500 kg × 26 SDR = 13,000 SDR | ≈ €15,000 (Estimated), still well short |

The gap is stark. Carrier liability is both capped and fault-based, so even a claim you win leaves most of the loss sitting with you. Cargo insurance works differently: it pays the declared or insured value (here, the full €40,000) regardless of who caused the loss. The figures above are Estimated, and the SDR rate fluctuates, so a live conversion will shift them. This is why most experienced shippers treat carrier liability as a backstop, not a safety net.

Cargo Insurance vs Carrier Liability: Which Clause You Need

Carrier liability is capped per kilogram and pays out only when the carrier is shown to be at fault, while cargo insurance pays the insured value of your goods regardless of fault, subject to its own clauses. That gap is why most shippers buy cover rather than rely on the carrier alone.

The level of cover is set by the Institute Cargo Clauses (ICC), the standard wordings used across marine cargo policies. ICC (A) is “all-risks” cover: the broadest protection, subject to a list of stated exclusions. ICC (B) and ICC (C) are named-perils cover, meaning they pay only for specifically listed events, with (C) the most restrictive and the cheapest.

The main exclusions under ICC (A) are:

- wilful misconduct of the insured

- ordinary leakage, loss in weight, or wear and tear

- inherent vice or nature of the goods

- delay

- war and strikes (unless added back by extension)

When a covered loss happens, insurance pays your declared value first, then the insurer pursues the carrier through subrogation (the insurer stepping into your shoes to recover from the party at fault). You collect on your value and avoid chasing a capped claim yourself. Match the clause to the cargo and the route: all-risks for high-value or fragile goods, named-perils where the risk profile is narrow.

Incoterms® 2020: Who Bears the Risk Files the Claim

The Incoterm fixes the exact point at which the risk of loss or damage passes from seller to buyer, and whoever bears that risk at the moment of loss is the party who should hold the cargo insurance and file the claim. The chosen Incoterms® 2020 rule decides who bears the risk, not who took out the insurance.

| Incoterm (2020) | Risk transfers at | Who bears transit risk / files |

|---|---|---|

| EXW | Seller’s premises (collection) | Buyer, almost the whole journey |

| FCA | When handed to the first carrier | Buyer, from handover |

| FOB / CFR / CIF | When goods are on board the vessel | Buyer, during the sea leg |

| DAP / DDP | Named destination | Seller, to destination |

Only two terms oblige the seller to insure: CIF (minimum ICC (C) cover) and CIP (upgraded to ICC (A) cover under Incoterms® 2020). Under CFR or FOB the buyer carries the sea-leg risk, yet the seller has no duty to insure, so the buyer needs to arrange its own cover. The common trap catches buyers on CIF who assume they are fully protected when the seller’s minimum obligation may be only ICC (C).

General Average: When You’re Billed for Someone Else’s Loss

Cargo that arrives untouched can still trigger a bill, under a maritime principle called “general average”. General average means that when cargo or property is deliberately sacrificed, or extra expense is incurred, to save the ship and the whole venture from a peril, every cargo owner contributes to that loss in proportion to the value of their goods.

The mechanics are straightforward once it is declared. The carrier can hold all cargo until each owner posts security: an average bond (Form A) from the cargo owner and an average guarantee (Form B) from their insurer. Would you have cash ready to release your own shipment? Adjustments can take two years or more to finalise. Cargo insurance covers your general-average contribution, so the burden falls on the insurer; a shipper without insurance must put up cash security to get their goods released.

How a Freight Forwarder Helps You File and Win the Claim

Most claims are lost on the dock, not in the paperwork. When a shipment goes wrong, the first hour of documentation usually decides whether the carrier pays. That is where we step in. Before your cargo even moves, we tell you which notification deadline applies to your lane (3, 7, or 14 days depending on mode), so the clock never catches you off guard.

On delivery, we coach the consignee on notating the transport document correctly, because a vague “received with damage” rarely holds up while a specific reservation does. Where the value justifies it, we arrange an independent survey to fix the cause and extent of loss on record. We then assemble the document pack and liaise with both the carrier and the cargo insurer, so the claim is filed cleanly and inside the window.

Low-volume shippers feel this most. An SME consolidating a pallet or two into a groupage load carries the same exposure as a full-container client but rarely has the staff to chase a claim alone.

[case study placeholder — typical scenario: a groupage shipment on a Balkan road lane arrives with two crushed pallets; we notate the CMR note at delivery, commission a survey within 48 hours, and file against the carrier and insurer before the 7-day CMR window closes]

Documents we help you gather:

- Bill of Lading, CMR consignment note, or air waybill

- commercial invoice (proves the value)

- packing list

- proof of delivery (POD) with the damage notation

- photographs of the damage and packaging

- survey report

- repair or replacement estimate

- insurance certificate / policy

Final Recommendation: Move Fast, Document Everything, Insure Properly

Three habits decide nearly every freight claim, and all three are within your control. Knowing what to do if your cargo is lost or damaged comes down to acting at delivery, respecting your deadline, and carrying the right cover before anything ships.

- Document at delivery: inspect the goods before you sign, notate the damage specifically, photograph it, and preserve the goods for survey.

- Hit the deadline for your mode: 3 days for concealed sea damage, 7 days for road under CMR, 14 days for air under the Montreal Convention.

- Insure properly: carrier liability is a capped backstop (roughly 2 to 26 SDR per kg), while cargo insurance pays out your declared value.

The gap between those two numbers is the whole argument for insuring. A claim filed late, or against liability limits alone, often recovers a fraction of what the goods were worth.

If you would like a quote with cargo insurance included, or you want to talk through your lane before you ship, the Sea Gate team is glad to help: sales@seagatelogistics.org or +359-886-476-414 (Telegram/WhatsApp).

Frequently Asked Questions

How long do I have to file a cargo damage claim?

Deadlines run by transport mode: 3 days for concealed sea damage, 7 days for road damage under the CMR Convention, and 14 days for air damage under the Montreal Convention. These notification windows are counted from the delivery or receipt of the goods. The separate time limit to actually sue is 1 year for sea and road claims and 2 years for air.

Who is liable if my freight is damaged in transit?

The carrier in care, custody, and control of the goods is liable, but only up to the cap set by the governing convention. To recover, the claimant must prove the cargo was tendered in good order and the loss happened in transit. A freight forwarder is generally liable only when it contracts as the carrier itself or acts negligently.

What’s the difference between cargo insurance and carrier liability?

Carrier liability is fault-based and capped by weight (around 2 to 26 SDR per kg depending on mode), so it rarely covers the full value of the goods. Cargo insurance pays your declared value regardless of who was at fault. Liability is a backstop; insurance is the actual financial protection.

How much will the carrier actually pay for lost cargo?

The carrier pays only up to the convention cap, not the invoice value. A €40,000 sea shipment lost at 2 SDR per kg might yield only about €1,200 to €1,300 (Estimated), depending on weight. That gap between cap and value is exactly what cargo insurance closes.

What documents do I need to file a freight claim?

You need the transport document (Bill of Lading, CMR note, or air waybill), the commercial invoice, and the packing list. Add the proof of delivery showing the damage notation, photographs, a survey report, and a repair or replacement estimate. Include the insurance certificate or policy if a cargo policy applies.

Do I have to note damage when I sign for delivery?

Yes, and the notation should be specific rather than a general “damaged” remark. Under CMR Article 30, if the consignee makes no reservation within 7 days, the goods are presumed to have been received in good condition. That presumption is hard to reverse, so written notation at delivery protects your claim.

Does cargo insurance cover general average?

Yes, your pro-rata general average contribution is covered under a standard cargo policy. The insurer issues the average guarantee (Form B) on your behalf, while you post the average bond (Form A) to release the cargo. This lets your goods move without you fronting a cash deposit.